Growing up is scary. Going from not having a care in the world to taking care of everything yourself can be a daunting task. Just paying the bills and buying groceries is enough, but when you start to think about savings and investment portfolios, the adult world can become overwhelming.

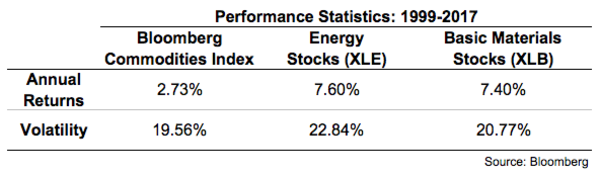

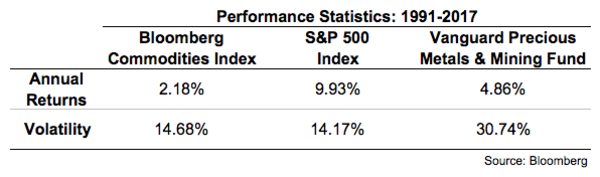

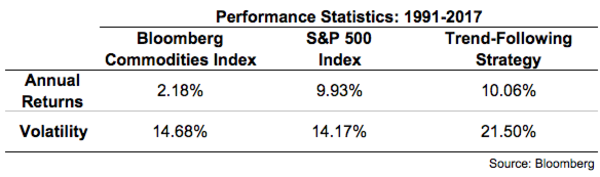

There’s your retirement fund—known as a 401K—at your job, of course. However, understanding how your 401K makes money can be a little confusing. Once you start thinking about how to invest your savings without help, personal finances can become a formidable proposition. According to NerdWallet, over 60 percent of people 18-34 are opting to use savings accounts to set money aside for retirement. If they set enough aside each month, they may still be in good shape come retirement. But if they invest, they could be significantly better prepared. If you are a risk-averse millennial that fears another stock crash like the mortgage crisis in 2008, technology may have an intriguing solution. The rise of cryptocurrencies such as Bitcoin, as well as safe ways to invest in them has led to an intriguing financial opportunity – cryptocurrency-based investment funds. What Is A Cryptocurrency? To explain what a cryptocurrency fund is, it is important to first understand the breakdown of the assets in the fund’s portfolio. Investing in cryptocurrencies such as Bitcoin, Ethereum, Ripple, and Dash is very similar to investing in currencies. People can use them for buying and selling and can invest in them as they would US Dollars or Euros. However, unlike their traditional counterparts, these cryptocurrencies have a limited supply, and they have to be “mined” in order to be used. Bitcoin became the first mainstream decentralized cryptocurrency in 2009. Since then, several others including Ethereum, LiteCoin and Dash have become increasingly popular, attracting new traders and investors thus increasing the overall market cap significantly. What Is A Cryptocurrency-based Investment Fund? The easiest way to describe a cryptocurrency-based investment fund is to compare it to its traditional counterpart, the classic investment fund. In a traditional fund, your money is allocated between several different investments. Some entail more risk than others, which of course brings more reward. The growth of your equity depends on the volatility of the market and the type of investments that make up the fund. Cryptocurrency funds operate in a similar fashion. eToro’s Crypto Copyfund, for example, is based on a diverse portfolio, currently allocating different percentages to six different cryptocurrencies (Bitcoin, Ethereum, Litecoin, Ripple, Dash, and Ethereum Classic), currently led by Bitcoin, and rebalanced on the first trading day of each calendar month. This fund focuses on cryptocurrencies with a market cap of at least $1 billion (with a roundup of up to 2%) and a minimum average monthly trading volume of $20 million. The weight of each of the CopyFund’s components is decided according by market cap, with a minimum of 5%. Other funds, such as those offered by Metis Management, prefer a more diversified investment portfolio, reserving part of their capital to invest in newer, more radical digital currencies. As cryptocurrencies have gained in popularity, cryptocurrency investment funds have opened the doors to respond to the increasing demand to trade these digital assets in a more regulated way. With several cryptocurrency exchanges operating around the world, cryptocurrency investment funds offer investors a relatively safe method to invest or trade in digital currencies and increase their exposure to a potentially high-value asset class. Are Crypto CopyFunds Worth the Investment? With most new investment trends, it helps to be in on the ground floor. While cryptocurrencies have reached a new phase in their maturity as an investment asset, it’s still possible to get excellent returns investing in them. The top 100 cryptocurrencies have already surpassed $100 billion in value, with Bitcoin accounting for the lion’s share. While they still hold more risk than traditional currencies and other assets, cryptocurrencies are becoming an established opportunity to diversify any investment portfolio. The value of each might remain volatile, but the popularity of cryptocurrencies is expected to continue to increase. Cryptocurrency investment and copy funds such as eToro’s can help investors mediate risk by providing a diversified and transparent way to spread capital amongst the best-performing cryptocurrencies for the highest returns. In addition, since this is a managed fund that updates on a monthly basis with the top cryptocurrencies, it provides a solution for investors interested in diversifying their portfolio with cryptocurrencies, but lack the time or knowledge to capitalize from them. While cryptocurrency prices will undoubtedly fluctuate in coming months and years, finding a way to safely invest and have exposure to one of the fastest-rising investment trends is a vital for forward-thinking traders. There are ways to access the asset class without investing directly in futures.  I recently wrote about how commodities are good for traders, but bad for investors as a useful long-term buy-and-hold financial asset. A broad basket of commodities has given investors lower returns than cash equivalents with higher volatility than stocks. That higher volatility means there will be cyclical swings where commodities see huge gains as well as huge losses. The question many investors should ask themselves is this: Is there a better way to invest in commodities since the long-term risk-reward profile is so poor? Commodities are a hedge against much higher inflation, so the past 30 years or so of disinflation haven’t been conducive to strong performance, but there are ways to access commodities in their portfolios without investing directly in futures. Own an index fund. The simplest way to gain exposure to commodities is to own a broadly diversified index fund. The SPDR S&P 500 ETF currently has around 6 percent of its holdings in energy stocks and another 3 percent in basic materials. Foreign stocks have an even higher commodities tilt. The iShares MSCI EAFE ETF has 5 percent in energy names and 8 percent in basic materials while the Vanguard FTSE Emerging Markets ETF has 7 percent and 9 percent, respectively. Invest in sector ETFs. You could also invest directly in these sectors. While this is a much more concentrated bet, ETFs now make it easier than ever to make a bet at the sector or industry level. Here are the returns since 1999 for the SPDR Energy ETF and the SPDR Basic Materials ETF compared to the Bloomberg Commodities Index:  Both funds have performed much better than commodities with similar volatility characteristics. The only problem with investing in sector funds is that they still have a fairly high correlation to the overall stock market. The correlations for XLE and XLB to the S&P 500 were 0.62 and 0.88 over this time frame. Many investors put their money into commodities in hopes of finding an uncorrelated portfolio diversifier, which sector funds may not provide. Invest in companies that mine commodities. Instead of owning the commodities themselves you could simply own equity in the companies that extract them and put them to use. The Vanguard Metals & Mining Fund does just that. Here are the stats in comparison to the S&P 500 and Bloomberg Commodities Index:  This fund had just a 0.05 correlation to the S&P 500 in this time, meaning there is virtually no relationship between the return streams. It also had better returns than commodities, but it did so with much higher volatility. It also comes with bone-crushing losses that can be similar to the underlying commodities:  There have been periods when physical commodities decouple from the equities of the mining companies but both are still quite cyclical. When looking at the types of losses and volatility involved in precious metals and mining stocks it makes for a difficult portfolio holding, even if it ends up providing valuable diversification benefits. Very few investors have the emotional stamina to hold through this type of volatility or rebalance into the pain when necessary. Stick to trend-following rules. Because of the cyclical nature of commodities they can work much better through the use of trend-following rules. Trend-following as an investment strategy seeks to follow the old maxim that you should allow your winners to run but cut your losers short. The goal of trend-following is to reduce volatility and the potential for large drawdowns. The following table compares commodities, stocks and a simple commodities trend-following strategy since 1991:  Our trend-following strategy in this example follows a simple 10-month moving average rule. Using the same Vanguard Precious Metals & Mining Fund, this strategy shows what would have happened if you would have held that fund when it was above its trailing 10-month moving average price and sold it to buy bonds whenever it dipped below the 10-month moving average.

Not only does a trend-following strategy cut the volatility by roughly one-third in this fund, but it also reduces the maximum drawdown in the fund from minus 76 percent to minus 33 percent by going to bonds as losses and volatility began to pile up. This example doesn’t include taxes or transaction cost but it does show how investors can use the cyclical nature of these securities to their advantage. The basic idea is to ride the momentum up when they are rising and try to get out of the way when they are falling, with the understanding that you can’t nail the timing perfectly in either direction. As you can see from the statistics, none of these strategies will be for the faint of heart. But investors do have options beyond investing directly in long-only commodity indexes if they would like to invest in this space.  1. Understand the technological risks.

Even Olaf Carlson-Wee (who was on the July cover of Forbes), the founder and chief executive officer of Polychain Capital, a $200 million crypto hedge fund that began with $4 million last September, says the number one thing he wants everyday investors to know is, “This is unproven technology and if you don’t know what you’re doing, you shouldn’t interact with tokens — from an investor and security perspective. If you’re naively coming in and saying, I’m going to speculate on this, you’re really going to get burned. It’s like playing against the casino; you’re going to lose, even if you win sometimes.” Crypto assets are not like regular money. They’re also a new technology, and you may not fully understand how to use that technology or, more specifically, secure your tokens. Tales abound of people who mined or otherwise obtained bitcoins back when they were worth almost nothing and stored them on old computers or thumb drives and then accidentally threw them out. (At least one unlucky soul even went to the dump to find his coins, which are worth $2,100 each today.) There’s also been a rash of thefts of bitcoins, ether and other tokens kept on centralized wallets and exchanges such as Coinbase or Xapo or Kraken or Poloniex (as opposed to user-controlled wallets) with hackers exploiting lax customer service agents at telcos, reseting victim’s passwords via text message and then transferring the victim’s crypto assets to the hacker’s own accounts. 2. Understand the business/economic risks. The other reason crypto investing is riskier than traditional investing has to do with the fact that it depends on an emerging field called crypto-economics — the game theoretic system that largely determines a coin’s success. Tokens are trying to create mini economies that have incentives that get the various actors within the system to not just keep it afloat but increase the value of the token. But designing one that actually does those things isn’t easy. Developers could create a coin that enriches only a few and disillusions everyone else, leading the community to abandon the network. Or the business could fail, in which case, demand for their token will plummet, along with the price. Or they could design a really successful business, but design the coin poorly so it doesn’t appreciate along with the adoption of the platform. At this point, it’s not entirely clear what will make any particular token valuable, and even the two frontrunners could easily lose their status — perhaps to some competitor not yet in existence today, a la Yahoo. Carlson-Wee’s advice? “Not to dabble in this with real stake. If you want to buy $10 of Ethereum, and poke around with smart contracts, I encourage that. But use it as a technology, not as an investment, unless you know what you’re doing.” 3. Understand the financial risks. According to CryptoCompare, Bitcoin is down 15% for the last week alone. Ethereum is down 22% over the same time period — and 54% over the last month. Trading your USD for BTC or ETH is not the same as exchanging it for GBP or euros. On June 11, in a Facebook group devoted to crypto trading, someone posted, “I’m strongly considering taking out a $15K loan (at 12% APR) to invest in ETH and BTC … Anyone want to convince me not to do it?” The first response, “Others might try to tell you to not pull out debt to invest, and while under normal circumstances that would be sound advice — these are not normal circumstances.” The comment got 23 likes. June 11 happened to also be the day ETH hit its peak, at $394.66. If that investor did indeed invest his 12% APR-borrowed money in ETH on that day, he would, by now, have suffered a 57% loss. Only put in what you can afford to lose — which excludes taking on any debt — and only allocate money you won’t need for a while, in case you do buy in at the top and need to sit through a downturn. 4. Understand the legal risks. Preston Byrne, a technology lawyer with expertise in virtual currencies, known for his view that tokens constitute securities, says, “There is the very distinct possibility that in 12 months’ time, some of [token sale holders] are going to be arrested and thrown into jail.” If that happens to a token you happened to invest in, your investment could very well tank. The Securities and Exchange Commission has not yet made a ruling on whether initial coin offerings are legal or whether tokens are securities. The only public statements any official has made were in May by Valerie Szczepanik, the head of the SEC’s distributed ledger group, who, speaking for herself and not the agency, said at industry conference Consensus, “Whether or not something is a security is a facts-and-circumstances based test. … You have to pick each one apart, and figure out what are the rights and obligations created by the coin, what are the economic realities, what are the expectations of the parties, what does the white paper say, how do these things actually work and what are their key features?” What she’s obliquely referring to here is the Howey test, which says that if the following four conditions are met, the offering is a security: It is (1) an investment of money, (2) in a common enterprise, (3) with an expectation of profit predominantly (4) from the efforts of others. To summarize a framework put together by wallet and exchange Coinbase, blockchain advocacy group Coin Center, VC firm Union Square Ventures and Ethereum project hub ConsenSys, token sales fit point 1. Whether or not it’s a common enterprise depends on factors like whether the network is live before the token sale or at least operational on a test network. If the crowdsale occurs only when the team has published a white paper but has no tech yet, then that makes the buyers dependent on the actions of the developers, which makes it less of a common enterprise and more like a security. An additional factor considered beyond the Howey test is whether the offering is structured less as a utility token (a token that gives users the ability to do something in the network) and more like a token that entitles the user to equity or a shared of profits. The latter are securities. (Listen to my podcast with Coin Center's Jerry Brito and Peter van Valkenburgh to hear more about the Howey test and what factors determine whether a token is a security.) Although numerous players, such as Carlson-Wee and USV partner Fred Wilson, have pointed out that regulators’ hands are somewhat tied because too draconian regulation could lead U.S. investors to flee to wallets and exchanges in other jurisdictions, where they will be even more vulnerable, that does not negate the fact that these investments come with a huge dose of regulatory uncertainty. 5. Understand that most projects will fail. Many observers believe the current frenzy in ICOs is similar to the internet bubble of the late ’90s (and it likely hasn’t even hit its most fevered pitch yet), which means the Pets.com, Webvan and Kozmo.com are currently among us or about to launch, but not identified. However, the Amazon and eBay of crypto could also be getting started right now. Fred Ehrsam, cofounder of Coinbase who left this past winter, says blockchain companies and protocols can form more quickly than C-corps, just as internet startups could form more quickly than pre-internet companies. He also believes these these protocols could be more valuable someday than any C-corp. However, he says, “For every one massive hit and three base hits, there are 100 failures. I don’t think the market is pricing that in at all. Right now all valuations are high. I think there’s going to be a serious shakeout, where there will be a few key and critical infrastructure tokens that are clear winners. There are also some tokens out there that are highly unlikely to succeed and those are wildly overpriced.” 6. If you’re still determined to invest in crypto, only do so if the rest of your financial life is in order. If, despite all these risks, you still decide to put your money in a highly speculative investment, Ford recommends you be living below your means, be debt-free, have an appropriate amount of emergency savings (usually, anywhere from three to 12 months’ worth of essential expenses depending on your personal circumstances), and be on track with big financial goals such as saving for retirement and your children’s college tuitions. "You have to be comfortable losing everything," she says. 7. Only put in as much as or less than you can afford to lose. The bulk of your investments should be in a “lockbox” — a “set it and forget it” diversified portfolio that acts as a piggy bank and that requires several steps from you before you can withdraw, says Kirsch. With this amount, you should be able to meet all your financial goals, such as amassing an adequate retirement nest egg, saving for your children’s college education or coming up with a down payment on a house. After that, depending on your net worth and how likely it is you will reach your goals, you could put anywhere from 1-10% of your net worth (only an amount you could lose but still meet your financial goals) into what he calls a “sandbox” — a diversified portfolio of riskier investments. In this case, he wouldn’t even recommend an investor put their full sandbox into crypto, even if it was invested in multiple tokens. Similarly, Naval Ravikant, cofounder and CEO of AngelList and venture partner of crypto hedge fund Metastable Capital, advises would-be speculators treat it like the speculative investment it is, while paying attention to fundamentals and trying to diversify. “The scammers are smarter than you,” he says. (In the cover story, he recounted that a token creator offered him a deal that would be considered illegal if it were for a security and that would give him a lower price than what was offered in the token sale.) “Take a very small amount of money, your throwaway money, treat it as if it’s already gone, you’ve mentally set it on fire, and put it in some distribution of a few truly legit layer 1 blockchains.” By that, he means tokens that fit into what Chris Burniske, the first buy-side analyst to focus exclusively on cryptoassets and author of the forthcoming book "Cryptoassets: The Innovative Investor’s Guide to Bitcoin and Beyond,” described in the cover story as crypto currencies and crypto commodities. For instance, some leading cryptocurrencies and commodities are Bitcoin (digital cash), Ether (gasoline for smart contracts), Zcash (privacy coin) and Monero (privacy coin). Another one that many experts believe has potential to become a foundational token is Tezos (smart contracts platform), but because the network isn't live yet and there's so much hype -- it raised the most of any crowdsale ever, plus got investment from VC Tim Draper -- this is the riskiest among this group of seeming safe bets. 8. Do your research so you understand what you’re buying. Read the white paper, join the Slack community, and research the development team. If you can’t find much information on them, then it’s not easy to hold someone accountable, whereas developers with strong reputations will want to deliver. It’s also best to choose projects that have a minimum viable product, to lessen the risk the token will be considered a security. Get a sense of the network’s game theory, and learn to evaluate the token separately from the business model, so you’re not stuck holding a token that won’t appreciate no matter how popular its platform gets. “Do your due diligence. Don’t buy because your neighbor is buying,” says Burniske. 9. Evaluate the crypto-economics. To find real value, look for a token that is integral to the function of the network and whose value should rise if the platform catches on. Stan Miroshnik, managing director of The Element Group, an investment bank for the cryptocurrency and token-based capital markets, who gets queries from Russia, Kazakhstan, Indonesia, Malaysia, countries in Latin America and all over the world, says he asks founders who come to him, “What purpose does a token have for your company’s ecosystem? Or is it something exogenous you’re creating just to access this funding environment?” You should be asking yourself the same — and avoiding any investments in the latter category. 10. Unless you’ve decided to day trade, don’t watch the price. Presuming that because of your research, you believe in your investment, and presuming that you could lose all the money you invested and still reach all your financial goals, you don’t need to watch the price of your investments every day. If you made a rational investment decision, then don’t let your emotions negate your hard work during a price swing. Kirsch recommends that his clients who have “sandbox” investments look only quarterly or semiannually and not make any immediate changes but give themselves a few days to think about it and then either leave their investments be or switch things up. “I’m not against checking your portfolio and making changes as long as it’s a process and not emotionally driven,” he says. This weekend, all cryptocurrencies suffered a blood bath. Now, this Monday morning, they’re all up. If you’ve decided to put your money in, make sure you have the stomach for what is certain to be a wild ride. |

RSS Feed

RSS Feed