|

As an old financial goat, I often get questions about aging from clients, seminar attendees and readers — even by email. I've no wondrous wisdom, but here are my 11 most offered tips that I sense few undertake:

1. Take seriously the need to finance a long life: You’ll likely live lots longer than you expect. Lifespans keep increasing and will continue to. In 1952 expectancy averaged 68.6 years. By 2006 it was 77.8. If you and your spouse are 65, odds favor one of you hitting 90. Maybe older! Invest as if you'll reach that milestone. Doing otherwise invites aged poverty. Little is more brutal. 2. Be clear early about family-support limits: Before it arises, decide with your spouse the limits on what you will and won’t do to support family members. Too much or too little causes bad outcomes. If the topic of support comes up, and you didn’t plan in advance, you will be too emotional and likely over or under give. Planning early saves relationships later. 3. Consider downsizing: Saves money, makes life more manageable, eases future burdens on offspring, but causes more upfront hassle and reduces guest potential (which may be good). 4. Consider upsizing: Big gatherings, room for lots of grandkids (nothing beats grandkids — get your kids to have more, which is the best tip of all). Negatives are higher cost and extra upkeep. 5. Consider moving closer to grandkids: Fun. And maybe you can coerce your no-good kids to do more for you. And if your kids are good — you will want them helping you as you age. All good. 6. If you can, involve offspring in your financial decisions: This requires that they are up to it. But the more you can do this, the less hostility will arise over time. And, as per above, you likely want and need their help eventually. Plus, you’ll learn a whole new side of them. 7. Drive the safest car you can: When I was young I hot-rodded. Now I know I can’t drive as well as I could (or thought I could). Time is against you. It only takes one idiot to ruin your life. That idiot could be you. My wife and kids were saved by her Volvo in the ‘80s in a head-on with a drunk. I came to love Volvo real fast. Cars are even safer now. Opt against the road idiot. 8. Build a cushion into your financial plan: Not everyone is highly disciplined about spending and planning. If you suffer a big gap between plans and realities, it causes anxiety — which makes for worse investors and hence worse results. Create an extra cushion year by year so at the end you aren’t trying to catch the ball with extremely shaky hands. 9. Know your net worth but don’t obsess over it: J. Paul Getty, when America’s richest man, famously said that really rich people hadn’t a close clue what they were worth because they owned illiquid assets that were impossible to price. If you aren’t rich, obsessing over exactly what you’re worth makes even less sense. Your sense of net worth is just a planning tool for the future. 10. Have a financial back-up person — or two: Whether you, a loved one or a professional, be clear who should oversee your finances if you’re numero uno choice can’t. If you ever need it, that decision made in haste and emotion could be as expensive as any. 11. Remember that anger slays: I got huge peace of mind when a psychologist buddy taught me to live my actions as if I’d live forever and my emotions as if I knew I’d be dead in 30 days. Every time I anger, I ask myself if I’d waste time over “this” if I knew I had only 30 days to live. I never do. It’s calming. Anger slays investors and you.  Managing your finances can be really stressful. There’s so much information to know, mastering all of it seems like an impossible task. Moreover, if you’ve developed some bad financial habits over the years, correcting them may seem extremely daunting.

Luckily, it is possible to improve your financial prowess. With a little effort, you will set yourself up for a better financial future, which can be a real benefit when it comes to starting a business. As you overcome your bad financial habits and instill new, good habits, you’ll learn how to manage not only your personal finances but business finances, too. If you want to become more successful and get closer to starting your own business, you need to give up the five habits below. Some of them you’ll be able to give up today, while others will take a little bit longer to overcome. There might be some hard work involved to rewrite these five behaviors, but once you do, you’ll find that the work was well worth the outcome. 1) Living paycheck to paycheck Very often, people have no idea what they’re actually spending all of their money on. Before they know it, their bank account is approaching zero, and they’re simply waiting for their next paycheck to come. The bottom line is this: without paying attention, it’s easy to spend the money you should be saving. If you’d like to break out of this vicious cycle, the first step is to start tracking your expenses. If you don’t know where all of your money is going, you can’t give it a purpose. So, track every dollar, understand how much is going in and how much is going out. With this information in mind, you can overcome the bad habit of living paycheck to paycheck. 2) Avoiding a budget Figuring out exactly how much money is coming in and going out is the first step to financial freedom, but it’s not the only step. Once you have a grasp of your monthly income and expenses, you’ll need to create a budget. Whether you’re managing your personal finances or your new company’s money, you should always have a budget in place. Creating a working plan that outlines how you’ll cover your expenses and save for the future is key to financial well-being. 3) Neglecting your credit score Knowing your current credit score and how you can improve it is paramount to success. Unfortunately, 30 percent of Americans have a bad habit of not checking and knowing their credit scores. Whether you worry about having bad credit or not, you should check your credit score at least once a year. Even if you are doing everything right, errors on your credit report might cause you to have an inaccurate score that threatens your financial health. Although neglecting your credit score is number three on this list, its importance shouldn’t be understated. When you start a new business, your credit will likely serve as your company’s credit history. To secure the best funding and financing available for your future company, you need to start managing and improving your personal score today. 4) Failing to review statements and bills Every month — sometimes several times a month — statements and bills roll in. Many of these documents don’t seem to require immediate attention, so people only view them at the end of the month. However, not opening these documents as soon as they arrive can wreak havoc on your finances. If you don’t view your statements when they arrive, you might miss out on important information that should inform your budget. Like your credit, it’s also not uncommon for incorrect items to make themselves onto your statements. Additionally, although you might dread looking at bills, you should catalog and categorize them as soon as they arise. Accidentally neglecting to pay a bill you’ve forgotten about is all too easy, so don’t give yourself the chance. This is a bad habit that doesn’t help your personal finances, and it certainly isn’t something you’ll want to do when you’re running your own company. 5) Thinking you can manage everything Many people — especially aspiring business owners — have a bad habit of thinking that they can do everything by themselves. There’s only so much you can learn about building, managing and preserving your finances. Fortunately, you can work with a mentor or a financial advisor that can help you overcome your bad financial habits to achieve financial freedom.  Over the years, mutual funds have come across as a popular and fairly profitable instrument of investment. They have proved to be more hassle free and risk averse as compared to direct stock investments.

Here is an insight on how you can plan your mutual fund investment: Short-term investment What? As the name suggests, these investments are made for short periods of time, typically for 12-month duration or even less. When? These investments are a boon in emergency situations. Be it a medical emergency or the sudden need of money for down payment of your car, short term mutual funds can bail you out. What to keep in mind? Since the investment is for a brief period, it needs to be ensured that your investment is insulated from market volatility. It is important as you would not want to see your investment numbers cut a sorry figure at the time of emergency. So, it is advised to invest in low-risk options -- liquid funds like Commercial Papers (CPs) and T-Bills or debt funds like government bonds, company debentures, fixed income assets etc. Mid-term investment What? These kind of mutual fund investments are made for a period of 1-3 years When? If you are planning to launch a start-up or a business, mid- term investments are your best bet. Experts say that these investments can be helpful in case you are planning to buy property or real estate. What to keep in mind? In mid-term investments, your aim should be to have the best of both worlds. That is, you should eye to maximize your capital gains but at the same time you cannot afford to take too much risk as the period of investment in this case, is still not very long. So you can choose to stick with debt funds or maybe opt for Systematic Investment Plan (SIP) or monthly investments. SIP in mutual fund is recommended as a great way for a salaried person to invest in equity markets for long-term basis without understanding the working of equity markets. Long-term investment What? Any mutual fund investment for a period of more than three years is termed as a long-term investment. When? As it is quite evident from the nature of the investment, long-term investments hold good if you are planning for the future. If you want to sort out your retirement plans, save for old- age health issues or nurture your child's education, you should definitely go for long-term investments. What to keep in mind? Since the investment is a long-drawn one, you can take down your guards off to some extent, against market volatility. You won't mind taking a few risks to rake in the maximum possible profits. So you can choose to invest in equity funds i.e. in shares of companies.  Growing up is scary. Going from not having a care in the world to taking care of everything yourself can be a daunting task. Just paying the bills and buying groceries is enough, but when you start to think about savings and investment portfolios, the adult world can become overwhelming.

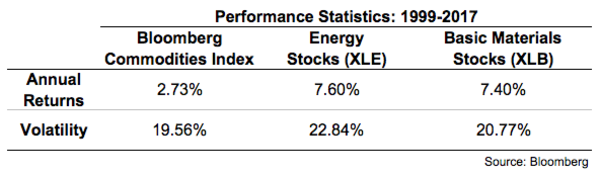

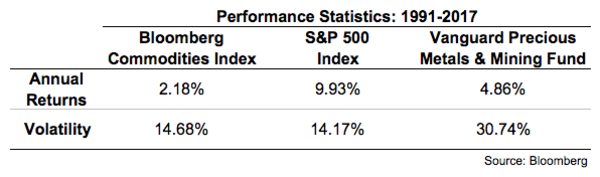

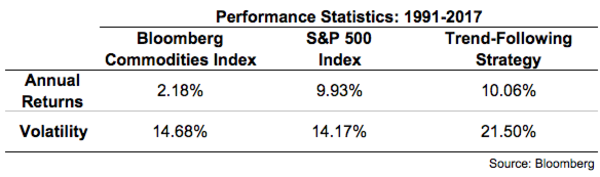

There’s your retirement fund—known as a 401K—at your job, of course. However, understanding how your 401K makes money can be a little confusing. Once you start thinking about how to invest your savings without help, personal finances can become a formidable proposition. According to NerdWallet, over 60 percent of people 18-34 are opting to use savings accounts to set money aside for retirement. If they set enough aside each month, they may still be in good shape come retirement. But if they invest, they could be significantly better prepared. If you are a risk-averse millennial that fears another stock crash like the mortgage crisis in 2008, technology may have an intriguing solution. The rise of cryptocurrencies such as Bitcoin, as well as safe ways to invest in them has led to an intriguing financial opportunity – cryptocurrency-based investment funds. What Is A Cryptocurrency? To explain what a cryptocurrency fund is, it is important to first understand the breakdown of the assets in the fund’s portfolio. Investing in cryptocurrencies such as Bitcoin, Ethereum, Ripple, and Dash is very similar to investing in currencies. People can use them for buying and selling and can invest in them as they would US Dollars or Euros. However, unlike their traditional counterparts, these cryptocurrencies have a limited supply, and they have to be “mined” in order to be used. Bitcoin became the first mainstream decentralized cryptocurrency in 2009. Since then, several others including Ethereum, LiteCoin and Dash have become increasingly popular, attracting new traders and investors thus increasing the overall market cap significantly. What Is A Cryptocurrency-based Investment Fund? The easiest way to describe a cryptocurrency-based investment fund is to compare it to its traditional counterpart, the classic investment fund. In a traditional fund, your money is allocated between several different investments. Some entail more risk than others, which of course brings more reward. The growth of your equity depends on the volatility of the market and the type of investments that make up the fund. Cryptocurrency funds operate in a similar fashion. eToro’s Crypto Copyfund, for example, is based on a diverse portfolio, currently allocating different percentages to six different cryptocurrencies (Bitcoin, Ethereum, Litecoin, Ripple, Dash, and Ethereum Classic), currently led by Bitcoin, and rebalanced on the first trading day of each calendar month. This fund focuses on cryptocurrencies with a market cap of at least $1 billion (with a roundup of up to 2%) and a minimum average monthly trading volume of $20 million. The weight of each of the CopyFund’s components is decided according by market cap, with a minimum of 5%. Other funds, such as those offered by Metis Management, prefer a more diversified investment portfolio, reserving part of their capital to invest in newer, more radical digital currencies. As cryptocurrencies have gained in popularity, cryptocurrency investment funds have opened the doors to respond to the increasing demand to trade these digital assets in a more regulated way. With several cryptocurrency exchanges operating around the world, cryptocurrency investment funds offer investors a relatively safe method to invest or trade in digital currencies and increase their exposure to a potentially high-value asset class. Are Crypto CopyFunds Worth the Investment? With most new investment trends, it helps to be in on the ground floor. While cryptocurrencies have reached a new phase in their maturity as an investment asset, it’s still possible to get excellent returns investing in them. The top 100 cryptocurrencies have already surpassed $100 billion in value, with Bitcoin accounting for the lion’s share. While they still hold more risk than traditional currencies and other assets, cryptocurrencies are becoming an established opportunity to diversify any investment portfolio. The value of each might remain volatile, but the popularity of cryptocurrencies is expected to continue to increase. Cryptocurrency investment and copy funds such as eToro’s can help investors mediate risk by providing a diversified and transparent way to spread capital amongst the best-performing cryptocurrencies for the highest returns. In addition, since this is a managed fund that updates on a monthly basis with the top cryptocurrencies, it provides a solution for investors interested in diversifying their portfolio with cryptocurrencies, but lack the time or knowledge to capitalize from them. While cryptocurrency prices will undoubtedly fluctuate in coming months and years, finding a way to safely invest and have exposure to one of the fastest-rising investment trends is a vital for forward-thinking traders. There are ways to access the asset class without investing directly in futures.  I recently wrote about how commodities are good for traders, but bad for investors as a useful long-term buy-and-hold financial asset. A broad basket of commodities has given investors lower returns than cash equivalents with higher volatility than stocks. That higher volatility means there will be cyclical swings where commodities see huge gains as well as huge losses. The question many investors should ask themselves is this: Is there a better way to invest in commodities since the long-term risk-reward profile is so poor? Commodities are a hedge against much higher inflation, so the past 30 years or so of disinflation haven’t been conducive to strong performance, but there are ways to access commodities in their portfolios without investing directly in futures. Own an index fund. The simplest way to gain exposure to commodities is to own a broadly diversified index fund. The SPDR S&P 500 ETF currently has around 6 percent of its holdings in energy stocks and another 3 percent in basic materials. Foreign stocks have an even higher commodities tilt. The iShares MSCI EAFE ETF has 5 percent in energy names and 8 percent in basic materials while the Vanguard FTSE Emerging Markets ETF has 7 percent and 9 percent, respectively. Invest in sector ETFs. You could also invest directly in these sectors. While this is a much more concentrated bet, ETFs now make it easier than ever to make a bet at the sector or industry level. Here are the returns since 1999 for the SPDR Energy ETF and the SPDR Basic Materials ETF compared to the Bloomberg Commodities Index:  Both funds have performed much better than commodities with similar volatility characteristics. The only problem with investing in sector funds is that they still have a fairly high correlation to the overall stock market. The correlations for XLE and XLB to the S&P 500 were 0.62 and 0.88 over this time frame. Many investors put their money into commodities in hopes of finding an uncorrelated portfolio diversifier, which sector funds may not provide. Invest in companies that mine commodities. Instead of owning the commodities themselves you could simply own equity in the companies that extract them and put them to use. The Vanguard Metals & Mining Fund does just that. Here are the stats in comparison to the S&P 500 and Bloomberg Commodities Index:  This fund had just a 0.05 correlation to the S&P 500 in this time, meaning there is virtually no relationship between the return streams. It also had better returns than commodities, but it did so with much higher volatility. It also comes with bone-crushing losses that can be similar to the underlying commodities:  There have been periods when physical commodities decouple from the equities of the mining companies but both are still quite cyclical. When looking at the types of losses and volatility involved in precious metals and mining stocks it makes for a difficult portfolio holding, even if it ends up providing valuable diversification benefits. Very few investors have the emotional stamina to hold through this type of volatility or rebalance into the pain when necessary. Stick to trend-following rules. Because of the cyclical nature of commodities they can work much better through the use of trend-following rules. Trend-following as an investment strategy seeks to follow the old maxim that you should allow your winners to run but cut your losers short. The goal of trend-following is to reduce volatility and the potential for large drawdowns. The following table compares commodities, stocks and a simple commodities trend-following strategy since 1991:  Our trend-following strategy in this example follows a simple 10-month moving average rule. Using the same Vanguard Precious Metals & Mining Fund, this strategy shows what would have happened if you would have held that fund when it was above its trailing 10-month moving average price and sold it to buy bonds whenever it dipped below the 10-month moving average.

Not only does a trend-following strategy cut the volatility by roughly one-third in this fund, but it also reduces the maximum drawdown in the fund from minus 76 percent to minus 33 percent by going to bonds as losses and volatility began to pile up. This example doesn’t include taxes or transaction cost but it does show how investors can use the cyclical nature of these securities to their advantage. The basic idea is to ride the momentum up when they are rising and try to get out of the way when they are falling, with the understanding that you can’t nail the timing perfectly in either direction. As you can see from the statistics, none of these strategies will be for the faint of heart. But investors do have options beyond investing directly in long-only commodity indexes if they would like to invest in this space.  1. Understand the technological risks.

Even Olaf Carlson-Wee (who was on the July cover of Forbes), the founder and chief executive officer of Polychain Capital, a $200 million crypto hedge fund that began with $4 million last September, says the number one thing he wants everyday investors to know is, “This is unproven technology and if you don’t know what you’re doing, you shouldn’t interact with tokens — from an investor and security perspective. If you’re naively coming in and saying, I’m going to speculate on this, you’re really going to get burned. It’s like playing against the casino; you’re going to lose, even if you win sometimes.” Crypto assets are not like regular money. They’re also a new technology, and you may not fully understand how to use that technology or, more specifically, secure your tokens. Tales abound of people who mined or otherwise obtained bitcoins back when they were worth almost nothing and stored them on old computers or thumb drives and then accidentally threw them out. (At least one unlucky soul even went to the dump to find his coins, which are worth $2,100 each today.) There’s also been a rash of thefts of bitcoins, ether and other tokens kept on centralized wallets and exchanges such as Coinbase or Xapo or Kraken or Poloniex (as opposed to user-controlled wallets) with hackers exploiting lax customer service agents at telcos, reseting victim’s passwords via text message and then transferring the victim’s crypto assets to the hacker’s own accounts. 2. Understand the business/economic risks. The other reason crypto investing is riskier than traditional investing has to do with the fact that it depends on an emerging field called crypto-economics — the game theoretic system that largely determines a coin’s success. Tokens are trying to create mini economies that have incentives that get the various actors within the system to not just keep it afloat but increase the value of the token. But designing one that actually does those things isn’t easy. Developers could create a coin that enriches only a few and disillusions everyone else, leading the community to abandon the network. Or the business could fail, in which case, demand for their token will plummet, along with the price. Or they could design a really successful business, but design the coin poorly so it doesn’t appreciate along with the adoption of the platform. At this point, it’s not entirely clear what will make any particular token valuable, and even the two frontrunners could easily lose their status — perhaps to some competitor not yet in existence today, a la Yahoo. Carlson-Wee’s advice? “Not to dabble in this with real stake. If you want to buy $10 of Ethereum, and poke around with smart contracts, I encourage that. But use it as a technology, not as an investment, unless you know what you’re doing.” 3. Understand the financial risks. According to CryptoCompare, Bitcoin is down 15% for the last week alone. Ethereum is down 22% over the same time period — and 54% over the last month. Trading your USD for BTC or ETH is not the same as exchanging it for GBP or euros. On June 11, in a Facebook group devoted to crypto trading, someone posted, “I’m strongly considering taking out a $15K loan (at 12% APR) to invest in ETH and BTC … Anyone want to convince me not to do it?” The first response, “Others might try to tell you to not pull out debt to invest, and while under normal circumstances that would be sound advice — these are not normal circumstances.” The comment got 23 likes. June 11 happened to also be the day ETH hit its peak, at $394.66. If that investor did indeed invest his 12% APR-borrowed money in ETH on that day, he would, by now, have suffered a 57% loss. Only put in what you can afford to lose — which excludes taking on any debt — and only allocate money you won’t need for a while, in case you do buy in at the top and need to sit through a downturn. 4. Understand the legal risks. Preston Byrne, a technology lawyer with expertise in virtual currencies, known for his view that tokens constitute securities, says, “There is the very distinct possibility that in 12 months’ time, some of [token sale holders] are going to be arrested and thrown into jail.” If that happens to a token you happened to invest in, your investment could very well tank. The Securities and Exchange Commission has not yet made a ruling on whether initial coin offerings are legal or whether tokens are securities. The only public statements any official has made were in May by Valerie Szczepanik, the head of the SEC’s distributed ledger group, who, speaking for herself and not the agency, said at industry conference Consensus, “Whether or not something is a security is a facts-and-circumstances based test. … You have to pick each one apart, and figure out what are the rights and obligations created by the coin, what are the economic realities, what are the expectations of the parties, what does the white paper say, how do these things actually work and what are their key features?” What she’s obliquely referring to here is the Howey test, which says that if the following four conditions are met, the offering is a security: It is (1) an investment of money, (2) in a common enterprise, (3) with an expectation of profit predominantly (4) from the efforts of others. To summarize a framework put together by wallet and exchange Coinbase, blockchain advocacy group Coin Center, VC firm Union Square Ventures and Ethereum project hub ConsenSys, token sales fit point 1. Whether or not it’s a common enterprise depends on factors like whether the network is live before the token sale or at least operational on a test network. If the crowdsale occurs only when the team has published a white paper but has no tech yet, then that makes the buyers dependent on the actions of the developers, which makes it less of a common enterprise and more like a security. An additional factor considered beyond the Howey test is whether the offering is structured less as a utility token (a token that gives users the ability to do something in the network) and more like a token that entitles the user to equity or a shared of profits. The latter are securities. (Listen to my podcast with Coin Center's Jerry Brito and Peter van Valkenburgh to hear more about the Howey test and what factors determine whether a token is a security.) Although numerous players, such as Carlson-Wee and USV partner Fred Wilson, have pointed out that regulators’ hands are somewhat tied because too draconian regulation could lead U.S. investors to flee to wallets and exchanges in other jurisdictions, where they will be even more vulnerable, that does not negate the fact that these investments come with a huge dose of regulatory uncertainty. 5. Understand that most projects will fail. Many observers believe the current frenzy in ICOs is similar to the internet bubble of the late ’90s (and it likely hasn’t even hit its most fevered pitch yet), which means the Pets.com, Webvan and Kozmo.com are currently among us or about to launch, but not identified. However, the Amazon and eBay of crypto could also be getting started right now. Fred Ehrsam, cofounder of Coinbase who left this past winter, says blockchain companies and protocols can form more quickly than C-corps, just as internet startups could form more quickly than pre-internet companies. He also believes these these protocols could be more valuable someday than any C-corp. However, he says, “For every one massive hit and three base hits, there are 100 failures. I don’t think the market is pricing that in at all. Right now all valuations are high. I think there’s going to be a serious shakeout, where there will be a few key and critical infrastructure tokens that are clear winners. There are also some tokens out there that are highly unlikely to succeed and those are wildly overpriced.” 6. If you’re still determined to invest in crypto, only do so if the rest of your financial life is in order. If, despite all these risks, you still decide to put your money in a highly speculative investment, Ford recommends you be living below your means, be debt-free, have an appropriate amount of emergency savings (usually, anywhere from three to 12 months’ worth of essential expenses depending on your personal circumstances), and be on track with big financial goals such as saving for retirement and your children’s college tuitions. "You have to be comfortable losing everything," she says. 7. Only put in as much as or less than you can afford to lose. The bulk of your investments should be in a “lockbox” — a “set it and forget it” diversified portfolio that acts as a piggy bank and that requires several steps from you before you can withdraw, says Kirsch. With this amount, you should be able to meet all your financial goals, such as amassing an adequate retirement nest egg, saving for your children’s college education or coming up with a down payment on a house. After that, depending on your net worth and how likely it is you will reach your goals, you could put anywhere from 1-10% of your net worth (only an amount you could lose but still meet your financial goals) into what he calls a “sandbox” — a diversified portfolio of riskier investments. In this case, he wouldn’t even recommend an investor put their full sandbox into crypto, even if it was invested in multiple tokens. Similarly, Naval Ravikant, cofounder and CEO of AngelList and venture partner of crypto hedge fund Metastable Capital, advises would-be speculators treat it like the speculative investment it is, while paying attention to fundamentals and trying to diversify. “The scammers are smarter than you,” he says. (In the cover story, he recounted that a token creator offered him a deal that would be considered illegal if it were for a security and that would give him a lower price than what was offered in the token sale.) “Take a very small amount of money, your throwaway money, treat it as if it’s already gone, you’ve mentally set it on fire, and put it in some distribution of a few truly legit layer 1 blockchains.” By that, he means tokens that fit into what Chris Burniske, the first buy-side analyst to focus exclusively on cryptoassets and author of the forthcoming book "Cryptoassets: The Innovative Investor’s Guide to Bitcoin and Beyond,” described in the cover story as crypto currencies and crypto commodities. For instance, some leading cryptocurrencies and commodities are Bitcoin (digital cash), Ether (gasoline for smart contracts), Zcash (privacy coin) and Monero (privacy coin). Another one that many experts believe has potential to become a foundational token is Tezos (smart contracts platform), but because the network isn't live yet and there's so much hype -- it raised the most of any crowdsale ever, plus got investment from VC Tim Draper -- this is the riskiest among this group of seeming safe bets. 8. Do your research so you understand what you’re buying. Read the white paper, join the Slack community, and research the development team. If you can’t find much information on them, then it’s not easy to hold someone accountable, whereas developers with strong reputations will want to deliver. It’s also best to choose projects that have a minimum viable product, to lessen the risk the token will be considered a security. Get a sense of the network’s game theory, and learn to evaluate the token separately from the business model, so you’re not stuck holding a token that won’t appreciate no matter how popular its platform gets. “Do your due diligence. Don’t buy because your neighbor is buying,” says Burniske. 9. Evaluate the crypto-economics. To find real value, look for a token that is integral to the function of the network and whose value should rise if the platform catches on. Stan Miroshnik, managing director of The Element Group, an investment bank for the cryptocurrency and token-based capital markets, who gets queries from Russia, Kazakhstan, Indonesia, Malaysia, countries in Latin America and all over the world, says he asks founders who come to him, “What purpose does a token have for your company’s ecosystem? Or is it something exogenous you’re creating just to access this funding environment?” You should be asking yourself the same — and avoiding any investments in the latter category. 10. Unless you’ve decided to day trade, don’t watch the price. Presuming that because of your research, you believe in your investment, and presuming that you could lose all the money you invested and still reach all your financial goals, you don’t need to watch the price of your investments every day. If you made a rational investment decision, then don’t let your emotions negate your hard work during a price swing. Kirsch recommends that his clients who have “sandbox” investments look only quarterly or semiannually and not make any immediate changes but give themselves a few days to think about it and then either leave their investments be or switch things up. “I’m not against checking your portfolio and making changes as long as it’s a process and not emotionally driven,” he says. This weekend, all cryptocurrencies suffered a blood bath. Now, this Monday morning, they’re all up. If you’ve decided to put your money in, make sure you have the stomach for what is certain to be a wild ride.  Do you consider yourself an investor? If you’re a woman, the answer is probably “no.”

Even women who easily manage their budget often are reluctant to embrace the idea of investing in the financial markets. But it’s probably even more important for women than men that they harness their money to the power of those markets. Here’s why: A confluence of factors is leading to a chasm in the amount of retirement income women have compared with men. Thanks in part to the gender wage gap and lower average Social Security benefits, plus smaller retirement-account balances, the median annual income of women 65 and older is 42% lower than men’s, according to a study by financial-services firm Prudential Financial Inc. The study is based on several data sources, including the U.S. Census and the Social Security Administration. The retirement-income gap is compounded, at least partly, because women often hesitate to embrace investing. And one reason for that is generally women want to feel completely knowledgeable before deciding on anything, whereas men tend to feel more comfortable winging it, according to an analysis of over 30 studies, cited by Prudential. Thus, for a lot of women, if they don’t feel they really know about investing, they’ll stay on the sidelines. Combine that desire for more knowledge with a lack of time—women spend an average of 28 hours a week on unpaid work, which is 65% higher than men’s average, according to Prudential— and the result is women failing to invest. “When it comes to investing, women’s shortage of time, combined with their desire for more information in decision-making, may fuel procrastination, lower engagement, and reduced confidence,” according to the Prudential study. Perhaps it’s no surprise, then, that even though the vast majority of married couples surveyed said they share financial decision-making, fully half of those couples also said that investing is the husband’s province, according to a survey by financial-services firm UBS, cited by financial adviser Alice Finn in her new book, “Smart Women Love Money.” Finn is founder and chief executive of PowerHouse Assets, in Concord, Mass. Yet there is no sexism or gender bias preventing women from investing, Finn notes. “It might be a long time before we close the gender wage gap or pass legislation to guarantee paid maternity leave,” Finn writes, “But you don’t need to wait for anyone else’s consent before you get more engaged in your financial future.” Finn also cites a Stash Invest survey that found that 60% of millennial women don’t see themselves as investors. “In actuality, an investor is anyone who puts money to work hoping to get a financial return,” she writes. Who among us doesn’t want our money to work for us? Too often I’ve heard women say that “personal finance is boring” or “investing is too complicated.” But having the money to reach our goals in life is not boring, and investing is definitely not complicated. So why not let the financial markets help us build our wealth, even as we spend most of our time enjoying our lives, careers, families, and adventures? Whether you’re trying to save through a 401(k) or other retirement plan at work, have a lump sum that you want to invest for the long-term, or are thinking that you’ve got $100 you could spare every month to invest for retirement, now’s the time to embrace the power of investing. Below is a brief rundown of how to start investing, culled from Finn’s book as well as a free investing guide produced by Ellevest, an online financial adviser (look for the guide on Ellevest’s website, under the Resources tab). 1. Start now What are you waiting for? “The sooner you get your money into the stock market, the sooner it can start working for you, year after year after year,” Finn writes. Finn is referring to the magic of compounding, which you should take advantage of immediately. Say you invest $10,000 and earn 10% on it in the first year. That gives you an extra $1,000. If you repeat that process the next year, you’ll earn another $1,000—plus $100 on the $1,000 you earned in the first year. That extra $100: that’s the magic. Your money builds on itself, and all you have to do is stay invested. If you have a retirement account at work, start diverting money from your paycheck. If not, go to a low-cost brokerage such as the Vanguard Group and open an account. Then put regular contributions on autopilot. If you qualify, you can open an IRA or Roth IRA to save for retirement, or you can open a regular (read: taxable) brokerage account. Or check out one of the so-called robo advisers: online advisers such as Ellevest (which has no minimum account balance and charges 0.5% of the money you invest, as a management fee). 2. Embrace stocks for the long haul Yes, the stock market is volatile and you may lose money on a short-term basis. That’s why you need to have a long-term outlook for any money you invest in the stock market. Staying in for the long haul lets you ride out the small bumps and even the larger market corrections. Consider that all the people who ran away from stocks during the most recent financial crisis: After the market hit bottom in March 2009, it then proceeded to boom. The S&P 500 SPX, +1.00% one measure of the stock market, is up about 258% since then. And what about the long-term outlook for the market overall? If you believe that companies in general will continue to innovate and grow, then you believe in the stock market’s ongoing success. Women might have a slight edge on men when it comes to investing for the long haul. “It’s about putting the money away and letting it grow,” says Sallie Krawcheck, co-founder and chief executive of Ellevest. “Women bring to the workplace and life in general certain characteristics that, on average, are different from men. One of them is they take a long-term perspective—and that is a real positive when it comes to investments.” 3. Make investing a habit As noted in Ellevest’s “5 Rules to Invest By,” it’s a smart idea to invest a small amount out of every paycheck. Investing on a regular, periodic basis helps you avoid the problem of market timing—that is, trying to figure out the best time to buy and sell stocks. With a regular investing habit, you buy throughout all market environments, whether the market is up or down, and you don’t sell until you’re just a few years out from needing the money. 4. Ask about fees When you invest, there’s more than one fee to watch for. First, if you hire an adviser, you’ll be paying that person in one form or another, so ask about management fees. Ellevest recommends not paying more than 1% of your total assets under management. Second, the investments you buy will charge a fee. Generally, mutual funds that track an index (both traditional mutual funds and exchange-traded funds) will be the cheapest way to invest. Third, ask about trading fees and any other charges. You want to shop around for low fees. Finn offers this example in her book: A $100,000 investment earning 6.5% a year over 30 years will become almost $500,000 if the investor pays a 1% annual fee. But if the fee is 2% a year, the end result is $375,000. 5. Diversify Investing doesn’t have to be complicated, and one reason is that you can pick index mutual funds, rather than getting distracted by all the various individual stocks. “Should I buy Apple AAPL, +0.13%? Should I buy Google GOOG, +0.03%? You can spend your whole life trying to figure out which individual stocks to buy, but you’re missing the big picture,” Finn says. She recommends investing in a low-cost portfolio of index mutual funds. Your next question is which mutual funds. “Asset allocation—how you divide up your assets—is your most important decision, not what individual stocks you’re going to buy,” Finn says. That is, what portions of your money will you put in stocks versus fixed-income assets such as bonds and cash. Within stocks alone, of course, there are many different categories, including mutual funds that focus on U.S. small-, mid- and large-capitalization stocks, international companies and many more. You don’t need a dozen mutual funds to invest for your future. For some ideas on which mutual funds to use for your long-term investing goals, check out MarketWatch’s Lazy Portfolios. And Finn’s book has a detailed guide to how to think about asset allocation. Finn also offers insights into any of what she calls the five fundamentals of investing: 1) investing in stocks for the long haul, 2) allocating assets, 3) using index funds, 4) rebalancing regularly, and 5) keeping fees low.  You must have taken a peek at this year’s billionaires who made it to the top of the list of those who added fortunes to their wealth. How many billions did they gain over the previous year’s figures?

Most investors think that having a high debt is undesirable and must be avoided. Naturally, they tend to see it as adding more risks to a company’s present exposures. And once that company defaults on its debts because of underperformance, it could fold up. Nevertheless, high debt can lead to positive consequences. It can bring in greater returns, even offsetting the greater risks involved in the process. Enhancing yields The major reason why debt can improve overall returns is because it costs much less than equity. A firm can raise capital either through equity or debt, with debt generally offering a less expensive option. Hence, maximizing a company’s debt levels in order to generate higher returns on equity is more logical. It can lead to greater profitability, stronger share-price performance and increased dividend growth. The proper circumstances Admittedly, maxing out a company’s debt levels is not a wise move at all times. Businesses with highly seasonal performance and dependent upon the conditions of the general economic environment might encounter great difficulties if their balance sheets are heavily leveraged. During times of low returns, they may not be able to undertake debt-servicing steps, aggravating the company’s situation. On the other hand, companies performing in sectors that offer strong, consistent and viable revenues should increase debt to comparatively higher levels to enhance the gains for their equity-holders. For instance, it is to the advantage of utility and tobacco firms to raise their debt levels because of their high level of earnings visibility and the relatively strong demand for their products. Economic periods During periods of low interest rates, it certainly makes sense for businesses to borrow as much as possible. The previous ten years provided such an opportune time to borrow, rather than to lend. Global interest rates have experienced such record lows, thus, leading many companies in various sectors to decrease their overall borrowing rates. In the future, a higher rate of inflation is expected, portending higher interest rates. Although it could lead to increases in the cost of servicing debt, it should be compensated somehow by higher prices passed on to the end consumer. Moreover, a higher inflation rate will serve to diminish the real-terms value of debt. This can lead to increased levels of borrowing in the future. Conclusion Although increasing debt levels can also increase overall risk, it can be a viable step under the proper conditions. During periods of low interest rates, businesses with strong business models may enhance overall revenues by raising debt levels. And while higher interest rates may entail rising costs of servicing debt in the future, higher inflation may reduce the real-terms value of debts. Hence, investors can opt to buy stocks with a modest degree of debt exposure to optimize their overall gains over the long-term.  For many years, value investing has grown to become a very popular and profitable investment strategy. Among those who consider value investing as a viable choice are Benjamin Graham and Warren Buffett – two of the most successful value investors with spectacular gains over a long period of time.

The expected returns from value investing are comparatively high, although the risks are oftentimes much higher than most investors can handle. This is because value investing can result in an investor being subject to value traps, which occurs when a stock’s price is low for a very valid reason. What are value traps? Value traps Surprisingly, value traps are more common than most investors realize. In spite of global share prices having increased from the beginning of the year, many other shares will still actively trade at significantly low prices in comparison to the broader index. Although some might catch up and recover, others will not. Nevertheless, low-priced shares commonly appeal to value investors since the capital gain potentials are attractive. In short, for a good number of conservative investors, value investing may provide a high-risk option which could bring a substantial loss. Beyond prices Value traps may indeed provide a trading risk for value investors who do not realize that “value” goes beyond merely having a low share price. According to Warren Buffett, “It is better to buy a great company at a fair price than to buy a fair company at a great price.” Ultimately, the viability of a company must be measured along with its share value. Hence, if a firm’s shares are selling at a lower price than their net asset value, a potential risk in the future might keep them from recovering the valuation deficit. Likewise, a stock which is valued according to the wider index may in reality provide significant value for money if there is a positive expectation of a rapid increase in returns over a medium-range period. In short, value investing can be a great strategy when you consider certain essential factors, such as price, prior to acquiring the shares of a company. Periodic changes Obviously, with rising stock prices, value investing loses its appeal. As investors all over are buying, value investors are selling and choosing to invest in other assets, such as cash. Conversely, when market prices are down, value investors will be buying stocks instead of selling them, contrary to the overall market consensus. Being a value investor then can be a challenging occupation; and, on the short-term basis, it is quite easy to suffer paper losses as past trends continue to prevail. However, on the long-term basis, it has proven to be a viable strategy for investors of a certain level of experience and capability. It is not totally risk-free. So, by not merely focusing on price, this approach can serve as a highly-dependable road to financial success in the long run. Passive Income Sources that Require an Initial Time Investment

Most of these sources will involve setting up a personal website or blog; but that is not actually an expensive proposition. You may utilize the services of Bluehost for this purpose. They will provide a free domain name and will host your blog at an initial price of only $3.95 monthly, a really cheap outlay for the opportunity to create a passive income source. Publish and Sell an eBook Online – Self Publishing has become a profitable source of income for many individuals. More often now, any eBook you buy from Amazon could be a self-published work. This is because self-publishing has become significantly easy; you should try it to find out how easy it really is. It simply involves writing and editing a book yourself, designing a nice cover for it and then submitting to a platform, such as Amazon’s Kindle Direct Publishing. Although there is no guaranteed success, that should not stop anyone from accomplishing one of the three proverbial things any person must do in life before passing on, besides having a child and planting a tree. And before that time does come, utilizing this passive income source requires plenty of marketing upfront before you can benefit from your investment. Offer an Online Course on Udemy – Udemy provides an online platform for people to take video courses on various subjects. You can be a producer instead of being a consumer on Udemy by offering your self-made video course and selling it online. This passive income source is a great option for those who have the skills or talents in any particular artistic or academic field. Moreover, it multiplies your efforts several times over, compared to the conventional one-on-one or classroom tutoring mode – indeed a potentially lucrative passive income source! Selling Your Photographs – Did you know that many websites, blogs and even magazines acquire their photos from websites featuring stock photos? So, if you are into photography, you can turn in your favorite shots to stock-photo sites and earn a fee each time someone buys one of your photos. License Your Music – In the same way, you can have your music licensed to bring you a stream of income through royalties paid by those who use your music. The usual venue for licensing music is through YouTube Videos, through ads and other means. Design an App – If you are a smartphone or tablet user, you are probably very familiar with apps downloaded into them. Perhaps, you yourself have a great idea for an app. In that case, get the help of a programmer to make that app for you. That should provide you some residual revenue. Affiliate Marketing – Affiliate marketing involves collaborating with a firm (becoming an affiliate) to receive a fee or commission on a product. This approach of creating income works well if you have a blog or a website. It might take a long period before you can build up the idea in order to gain passive income from it. Check out affiliate marketing programs available online to find out which suits your needs best. Network Marketing – Network marketing, also referred to as multi-level marketing, has been drawing people for many decades now and providing many of them with above-average income. You have probably heard of such firms as Avon, Young Living Oils, Pampered Chef and AdvoCare -- all engaged in multi-level marketing. This can be a great source of passive income. You can build a team to work under your banner (what is called your down-line people) who will provide you commissions from the sales they make, even if you do not make any sales at all or just make a token sales output based on your required quota as one team. Design and Produce T-Shirts – Cafe Press provides online users to make their own T-shirt designs or other items requiring some designing work. You can earn royalties from the designs you make, especially the ones that become hits. Sell Digital Files on Etsy – You can also sell your own artwork through Etsy which provides digital files of artwork people can print out for decorating purposes. Other popular digital files on Etsy are available for download. Who knows? Your collection of graphic designs might provide you a steady stream of passive income if you join the site. Ideas for Semi-Passive Small Business Ventures Vending Machines – Vending machines can be a fantastic low-maintenance small-enterprise venture. Any individual can maintain several vending machines in a string of nearby towns. Every two weeks, you can collect and refill them, bringing revenue for your future retirement life. Car Wash – There are still many places that do not have car washes. It is a good semi-passive income source. A weekly regular maintenance job can provide a very comfortable schedule for a business idea that you can either personally manage or hire out to someone else. Storage Rentals – You can also rent out to customers storage space for a monthly income. The main job involved is when opening any of the storage units for new customers. Laundry Services – This is a rather debatable option for a semi-passive income source since it can actually involve a lot of continuing maintenance work. You can decide whether it is worth all the expected work. Easy Passive Income Sources Finally, here are a couple of easy passive income sources which demand no cash and no initial work. Although the returns are very minimal, nothing beats getting easy passive earnings. Cashback Rewards Cards – Using a credit card to pay bills can provide you cash-back rewards. Allowing your rewards to accumulate for a certain period and later putting the easy money you saved into a passive income venture will do the trick for you. (Check if the card you use does not charge a yearly fee; or else you end up with zero revenue in the end.) Cashback Sites – Similar to the previous one, you can choose to use a cashback site when shopping online. Why should you not get a hold of that free money for so little or for no work at all? You may decide between eBates and TopCashBack, the two most popular sites available. Get Started Now The best strategy for a beginner is to have only one passive income source instead of having 4 or 5 right away. This allows you to learn slowly the ropes first and to focus on building a passive income venture. Once you have mastered one, add another until you are fully content with the income stream you have built up. At the start, a significant amount of money and time will be involved; however, in time you will realize that earning passive income is a cinch! Choose the most suitable idea, plan your venture and commit yourself to that income source until you start benefitting from it. |

RSS Feed

RSS Feed