Sometimes, people who aspire to be business owners have this idea that they’ll pitch their idea, get millions of dollars in funding and start spending money like pro athletes. But, if they’re anything like the average American, they'll have an average $1,000 in savings (if that).

They’ll also have $17,000 to $137,000 in debt. If these numbers describe you, then borrowing money, applying for a loan, relying on credit cards and finding an investor may not be your best move. Instead, you should bootstrap your business. My co-founder Dan Foley and I bootstrapped Tailored Ink back in August 2015. We spent a combined $1,000 to get it off the ground and kept our costs low. Flash-forward to today, two years later and we’re swiftly closing in on the $1 million mark. We still haven’t maxed-out our credit cards or applied for a business loan. Want to know how we did it? Here are some financial habits we learned on our way to becoming successful business owners. 1. Spend within your means. When I was making $40,000 a year, back in 2012, I was eating frozen TV dinners every single night. Aside from my desktop computer, which cost only $300, there was no furniture in my apartment to speak of. I even slept in a $25 inflatable bed. Most of my friends and colleagues who had tons of college debt and were making about the same as me were literally pissing money. When they ran out of cash, they would max-out their credit cards. Despite everything you may have seen on TV, this is not how to behave if you want to become successful. You’ll never accumulate wealth if you spend it as soon as you get it. Debt and loans do not equal wealth. How do you keep yourself disciplined and spend less money in a credit-dependent and debt-ridden culture? By practicing delayed gratification. It’s the key to financial success. You need to believe that your short-term sacrifices will result in long-term gain. And they will. 2. Save way more than you spend. With that in mind, you should aim to save as much as possible. Some people will tell you the exact opposite, as in, “Don’t worry about saving until you’re 30.” These are the same people who'll work until they’re 65 and wonder why their savings accounts are so small. There are plenty of secrets to growing money, but there’s no secret at all to saving it. You just need to tuck in your belt and control your spending. Many financial advisors recommend saving at least 10 percent of income per year, but that’s not enough if you want to be rich one day. Saving as a business owner is even trickier because you'll have other people to think about. Let’s say you make $10,000 a month at your new business. That sounds pretty great -- but after you pay 20 to 40 percent of that revenue for tax, 25 percent for business expenses and 25 percent for living expenses. . . There won't be a whole lot left. If you’re running a B2B business, you'll also have accounts receivable to think about. Not all of your clients will pay you on time, if at all. Dan and I save way more than we spend and put most of what we make back into the business. That way, we can afford to pay all our vendors before we pay ourselves. We keep a two-month runway in our business bank account at all times. 3. Always pay off your debts (or don’t borrow at all). America has a serious credit problem. We’re brainwashed into believing that borrowing huge sums of money on a regular basis is smart. That’s why we do just that for college, cars, houses and even businesses. It’s why Americans had nearly $1 trillion in credit card debt back in 2015. If you really stop and think about it, though, this is insane. Warren Buffett has some pretty strong opinions about debt and loans. “You don’t really need leverage in this world much," he said. "If you’re smart, you’re going to make a lot of money without borrowing.” Buffett indicated that he was especially leery of credit cards. “Interest rates are very high on credit cards," he said. "If I borrowed money at 18 percent or 20 percent, I’d be broke.” So, just as an example, let’s say you charged $5,000 to your credit card with an APR of 15 percent, and you paid the minimum 2 percent each month. After 14.3 years, you’d have paid out an additional $5,614.44 -- more than you borrowed. 4. Don’t just leave your money in the bank. Speaking of savings accounts, they’re pretty much worthless. The interest rates at nearly all banks are so low that they’re insulting. Yet most people continue to think that leaving money in the bank is the safest thing they can do. But you have other, better options. Nearly all banks and brokerages give you similar insurance -- just through different providers. Banks give you insurance for up to $250,000 in cash from the FDIC, while brokerages have the same coverage through SIPC. In other words, as long as you have less than $250,000, your savings are just as safe in a brokerage as they are in a bank. You can trade stocks, bonds and funds without worrying that someone will steal your money. And if you follow Warren Buffett’s low-risk advice to invest in different index funds, you can earn upwards of 5 percent to 10 percent per year. The S&P 500 Index, for example, returned an average of 11.69 percent per year in the year’s from1973 to 2016. Compare that to 1 percent, which is the highest interest rate generous banks offer. What’s in your wallet? Bootstrapping a business isn’t that hard. You just need a basic understanding of how wealth accumulation works, and accept that your money-spending habits may not currently be aligned with success. That’s the hard part. But if you dream of owning your own successful business one day or becoming a millionaire before you retire, you’re going to have done some soul searching. Are you willing to delay your gratification and make some sacrifices in the near future so you can reap the rewards down the road? Will that sacrifice be worth it to you?  When we're young, we tend to think about retirement as though it's just a really long, really great vacation.

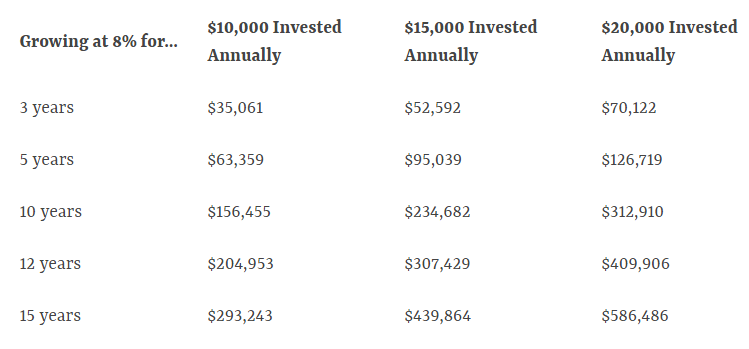

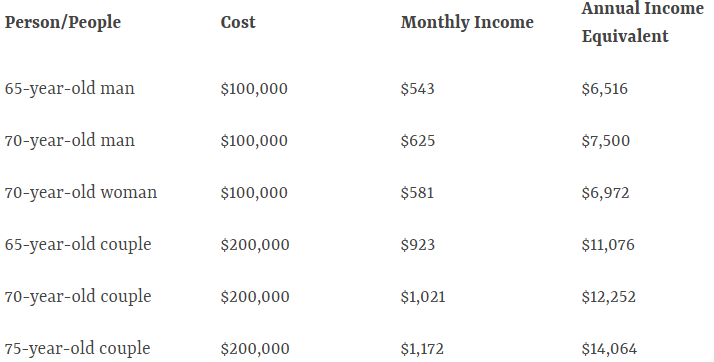

We picture a house near the beach or a golf course. We can get out of bed when we please, stay up all night if we want, and never worry about another missed deadline. A frosty beverage is always at hand, and there's a hammock waiting in the shade. But as we grow older and retirement gets closer, that enthusiasm often turns to angst. We have to figure out how the heck we're going to pay for the lifestyle we want when the paychecks stop -- and that can be a challenge, even for the savviest of savers. Here are six mistakes to avoid when planning your dream retirement: 1. You do not have a plan. Your No. 1 goal in retirement should be to know how much you will have coming in each month from all of your income streams -- and how you'll make that money last. Most prospective clients I meet with have a broker who helps them choose and purchase investments, but they don't have a holistic, written retirement plan that covers five key areas: · Income (how you will pay yourself) · Investments (how you will keep growing your money while also keeping it safe) · Taxes (how you will hold onto more of the money you worked so hard to save) · Health care (how you will deal with the short- and long-term care expenses that could significantly reduce your nest egg as you grow older) · Estate (how your spouse, children and favorite charities will be taken care of when you die) Your plan is your guide to and through a successful retirement. 2. You have never had your portfolio stress-tested. One of the first questions I ask clients is how much money they're willing to lose if there's a market downturn. They always say zero. Of course, that isn't an option in investing; to earn a return, you must take on some risk. But we usually can land on an amount they can handle, both financially and psychologically. Software (such as the Riskalyze program we use) can help determine your risk tolerance -- and whether that's what your current portfolio is built for. Most people are surprised to see how aggressive their investments are compared with their comfort level. This can be fixed -- but first, you have to know where you stand. 3. You do not have a tax plan. Investors often underestimate how much they will pay in income taxes after they retire. Some aren't aware that up to 85% of their Social Security benefits can be taxed. Others forget that Uncle Sam owns a portion of their 401(k) or IRA if they aren't in a Roth account, and when they take out their money, they'll have to pay him his share. Many are under the (usually mistaken) impression that they'll be able to live on far less income during retirement. I recommend working with a CPA who understands retirement income tax planning. And it's always a plus if your financial adviser and tax professional are working as a team to maximize tax efficiency. 4. You have an unrealistic income plan. Many of the income plans my prospective clients come in with use a high rate of return that, at best, is a reach; they use minimum inflation protection rates and low tax rates; and there are no assets set aside for health care costs. A plan like that could leave you in a vulnerable situation. I prefer to build a more conservative plan, and if it turns out you have more money to work with than you thought, its gravy. 5. You do not understand investment fees. Most investors don't know how much they pay in fees, which can be layered and complicated. When we run software to identify those fees, we find some people are paying as much as 3%. That may not seem like a lot, but if you look at a $1 million portfolio with an 8% rate of return over a 30-year period: · A portfolio with 3% in annual fees will have $4.0 million. · A portfolio with 2% in annual fees will have $5.5 million. · A portfolio with 1% in annual fees will have $7.4 million. The power of compounding interest is a beautiful thing -- and you want to make the most of every penny you put away. Pay attention to your prospectus, and don't be afraid to ask about fees. Your vigilance could save you thousands or even millions of dollars over the course of your retirement. 6. You do not have an estate plan, or you don't update it regularly. If you don't have an estate plan, the state in which you live has one for you -- and it likely won't be anything close to what you wanted for your loved ones. Again, it's best if your adviser is working with a CPA and an estate-planning attorney. Most people need a will, a living will and a power of attorney, which should cost around $400 to $600, depending on the attorney. You also may need or desire to draw up a trust. If your legacy is an important part of your retirement dream, your wishes should be included in your comprehensive plan. If you're closing in on retirement -- or if you're already there -- putting together your written plan should be a priority. And if you've been fretting, knowing that you have a guide to go by can make your retirement dreams feel a little more doable. Just make sure your adviser includes a way to pay for the occasional umbrella drink and at least one big comfy hammock.  According to the 2017 Retirement Confidence Survey, about 24% of workers said they had less than $1,000 saved for retirement, and a whopping 55% had less than $50,000. Only 20% had socked away $250,000 or more -- and even that seemingly hefty sum won't provide for the comfiest of retirements. Clearly, many of us have not set ourselves up to have the money we'll need in retirement. Fortunately, though, there are some ways to get more money in our golden years. Here are seven ways you can get more money in retirement. 1. Work a little longer before retiring Most people probably don't want to put off retiring, but it can be a very effective strategy, giving you a bigger nest egg to retire with and fewer years that it will have to last. You might enjoy your employer-sponsored health insurance for additional years, too, perhaps while collecting a few more years' worth of matching funds in your 401(k). Not convinced it's worth it? Well, imagine that you save and invest $10,000 per year for 20 years and it grows by an annual average of 8%, growing to about $494,000. That's pretty good. But if you can keep going for another three years, still averaging 8%, you'll end up with more than $657,000! That's more than $160,000 extra just for delaying retiring for a few years. If you're somewhat close to retiring, the table below will show you how much more you might amass over several time periods if your money grows by an annual average of 8%:  2. Work a little -- in retirement Whether you delay retiring or not, you should consider working a little while retired. Sure, it might seem to defeat the goal of living work-free, but many retirees actually find that they miss the structure and opportunities for socializing that their job provided. Many find themselves restless and a bit lonely in retirement, and a low-stress job on the side can be quite helpful. Working just 12 hours per week at $10 per hour, for example, will generate about $500 per month -- a useful sum. If you're imagining being a cashier at a local retailer or delivering newspapers and you're not excited by that, think a little harder about work possibilities. You might do some freelance writing or editing or graphic design work. You might tutor kids in subjects you know well, or perhaps give adults or kids music or language lessons. You might do some consulting -- perhaps even for your former employer. You could babysit, walk dogs, or take on some handyman-type jobs. These days the internet offers even more options. Make jewelry, soaps, or sweaters and sell them online. 3. Get -- and stay -- debt-free When you're living on a reduced income, it will be extra hard to pay off credit card debt or other high-interest debt, and those payments can hurt your ability to make other necessary payments. Paying off your debt before you retire will leave you with more money. It can be OK to be still carrying a mortgage in retirement, but many people aim to have their homes paid off before retiring. Credit card debt is a different matter, though, as it can be financially devastating. Aim to pay that off pronto, no matter whether you're in retirement or are only 37 years old. It's not unusual to be charged annual interest rates of 25% or more, and on $8,000 of debt, that can cost you around $2,000 each year! 4. Make the most of retirement savings accounts The more you contribute to tax-advantaged retirement savings accounts such as IRAs and 401(k)s, the more money you'll have in retirement. There are two main kinds of IRA -- the Roth IRA and the traditional IRA -- and for 2017 and 2018 alike, the contribution limit for both kinds of IRAs is $5,500 for most people and $6,500 for those 50 and older. Meanwhile, a 401(k) has much more generous contribution limits -- for 2017 it's $18,000 for most people and $24,000 for those 50 or older, and for 2018 it rises to $18,500 for most people, while the $6,000 catch-up limit is unchanged. Those contribution limits might not seem like a lot of money, but they're quite powerful if your money can grow for many years. As an example, socking away $5,000 annually for 25 years will get you nearly $400,000 -- and you'll likely be able to invest larger sums over time, as you earn more and contribution limits rise. Roth IRAs and Roth 401(k)s (which are increasingly available) can be especially powerful retirement income generators, as they let you withdraw money in retirement tax-free! 5. Buy fixed annuities Another good way to set up regular income for you in retirement is through annuities. Yes, some annuities, such as variable annuities and indexed annuities, can be quite problematic, often charging steep fees and sporting restrictive terms. But another kind -- fixed annuities -- is well worth considering. They're much simpler instruments and they can start paying you immediately or on a deferred basis. Below are examples of the kind of income that various people might be able to secure in the form of an immediate fixed annuity in the current economic environment. (You'll generally be offered higher payments in times of higher prevailing interest rates.)  Annuities remove worries about stock market moves and the economy's current condition and keep paying you no matter what is going on in the economy. A deferred annuity can also be smart, starting to pay you at a future point, such as when you turn a certain age. A 60-year-old man, for example, might spend $100,000 for an annuity that will start paying him $957 per month for the rest of his life beginning at age 70. Deferred annuities are a good way to avoid running out of money late in life.

6. Borrow against your life insurance Here's a retirement-income strategy many don't think of: Borrow against your life insurance. This can work if you've bought "permanent" insurance such as whole life or universal life. It won't work if you've bought term life insurance that generally only lasts as long as you're paying for it. (A note to insurance buyers, though: Term insurance is preferable in many ways.) You'll be reducing or wiping out the value of the policy with your withdrawal(s), but if no one really needs the ultimate payout, this strategy can make sense. Plus, the income is often tax-free. 7. Make the most of Social Security Finally, think strategically about Social Security. You can increase or decrease your benefits by starting to collect Social Security earlier or later than your "full" retirement age (which is 66 or 67 for most of us), and you can get more out of the program by coordinating with your spouse when you each start collecting. For example, if you and your spouse have very different earnings records, you might start collecting the benefits of the spouse with the lower lifetime earnings record on time or early, while delaying starting to collect the benefits of the higher-earning spouse. That way, you both get to enjoy some income earlier, and when the higher earner hits 70, you can collect their extra-large checks. Also, should that higher-earning spouse pass away first, the spouse with the smaller earnings history can collect those bigger benefit checks. There are even more ways to maximize your Social Security income -- so learn more about them and see which ones you can act on. It's often assumed that retirees live on fixed incomes, but that's not entirely true. Social Security checks are increased over time, and there are many ways to increase the income you expect to be living off of in your golden years. Much of your future financial security is under your control. The $16,122 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $16,122 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after. |

RSS Feed

RSS Feed